Modular vs. Manufactured vs. Mobile Homes: What’s the Difference?

Comparing modular, manufactured, and mobile homes can get confusing because the terms are often used interchangeably. They’re all connected to factory-built housing, but they don’t follow the same rules, use the same foundations, or fit the same financing path.

The biggest differences come down to building code, permanent chassis, foundation type, financing, insurance, and long-term value. Once you understand those basics, it’s easier to compare your options and decide which home type fits your land, budget, and plans.

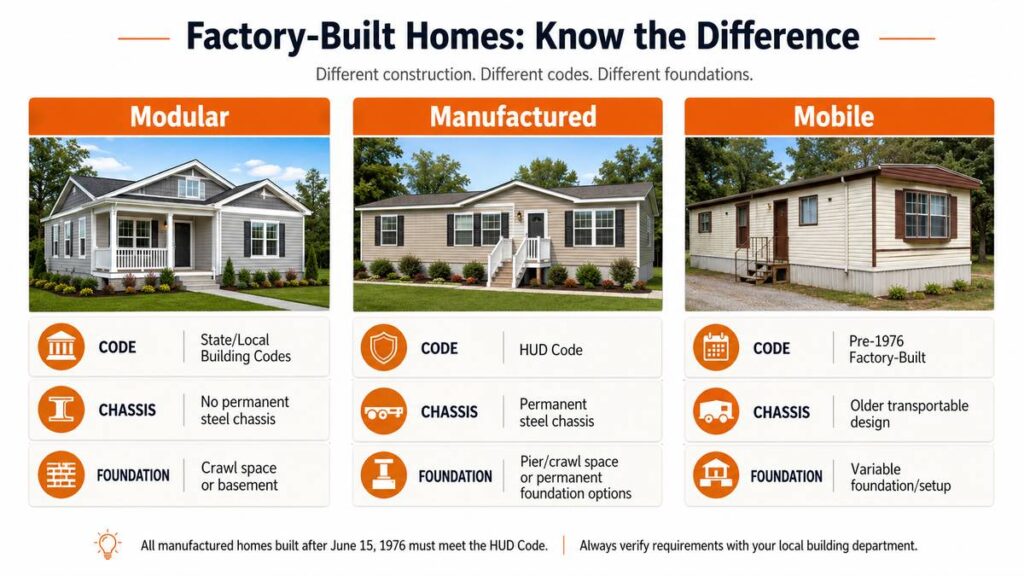

TL;DR: Modular homes, manufactured homes, and mobile homes are all tied to factory-built housing, but they aren’t the same. Mobile homes usually refer to older factory-built homes made before modern HUD standards. Manufactured homes are built to federal HUD Code and typically include a permanent steel chassis. Modular homes are built in sections, set on a permanent foundation, and follow state and local building codes like site-built homes.

The main difference is the building code

The clearest way to compare mobile, manufactured, and modular homes is to look at the building code that governs each type. The code affects how the home is classified, how it’s inspected, what type of foundation it may use, and how lenders or insurers may view it.

Mobile homes refer to older factory-built homes

A mobile home usually means a factory-built home built before June 15, 1976, when modern HUD standards took effect. People still use the term casually for newer manufactured homes, but technically, it points to an older category of factory-built housing.

That distinction matters because older mobile homes may be harder to finance, insure, move, or place on certain properties.

Manufactured homes follow HUD Code

A manufactured home is built in a factory to federal HUD Code standards. These standards cover areas such as construction, safety, energy efficiency, electrical systems, plumbing, heating, cooling, and installation.

Manufactured homes typically include a permanent steel chassis. They may be installed on pier systems, crawl spaces, or permanent foundations, depending on the home, property, local requirements, and financing path.

Modular homes follow state and local building codes

A modular home is also built in a factory, but it follows the same state and local building codes as a traditional site-built home. It’s delivered in sections, assembled on-site, and placed on a foundation.

Because modular homes follow local building codes and do not have a permanent chassis, they’re generally treated more like site-built homes for financing, insurance, and resale.

Construction and foundation differences that buyers should compare

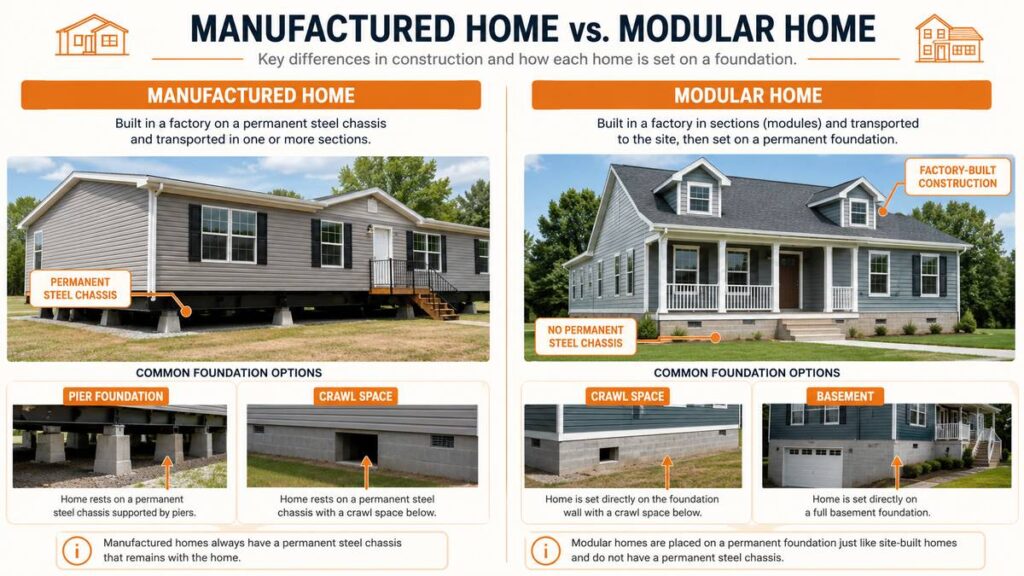

Modular and manufactured homes both start in a factory, but the path changes once the home reaches the site. The main construction difference is whether the home has a permanent steel chassis and what type of foundation it’s designed to use.

Factory construction is the shared starting point

Both home types are built indoors before delivery, which helps protect materials from weather during much of the build. After delivery, the home is set on the property and finished based on its classification, site conditions, and local requirements.

That controlled factory setting can make the building process feel more predictable. The site still needs to be ready before the home can be placed, connected, and completed.

Chassis and foundation affect classification

A manufactured home usually includes a permanent steel chassis as part of the structure. It may be installed on pier systems, crawl spaces, or permanent foundations, depending on the home, property, lender, and local requirements.

A modular home does not have that chassis. It’s delivered in sections, placed on a crawl space or basement foundation, and finished on-site more like a traditional home.

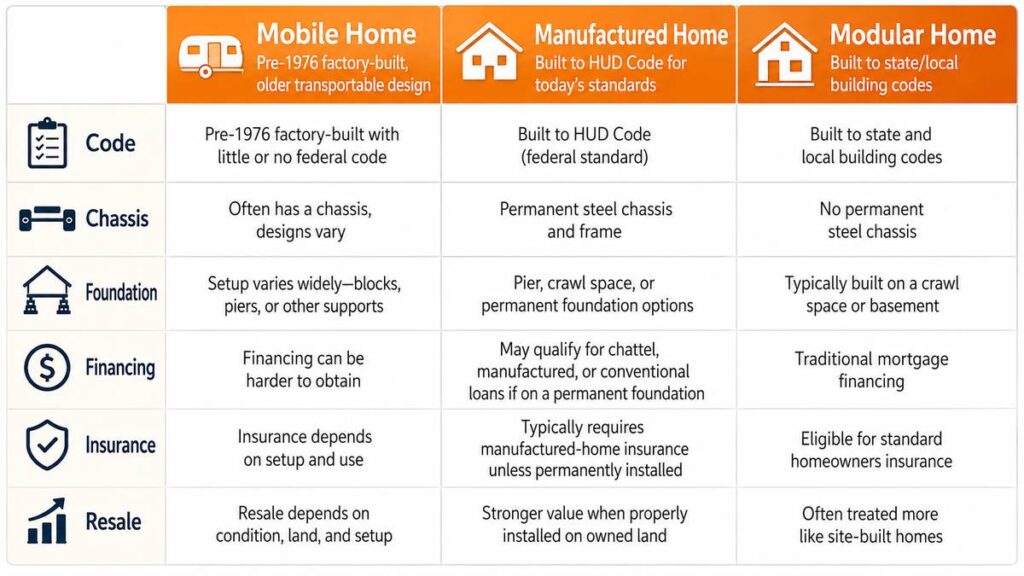

How modular, manufactured, and mobile homes compare

The biggest differences between modular, manufactured, and mobile homes show up in code, foundation, financing, insurance, and resale. Those details can affect what you can build, how the home is placed, and how lenders or insurers classify it.

| Comparison point | Mobile home | Manufactured home | Modular home |

|---|---|---|---|

| Code | Usually refers to factory-built homes made before June 15, 1976 | Built to federal HUD Code | Built to state and local building codes |

| Chassis | Often associated with older transportable designs | Typically includes a permanent steel chassis | No permanent steel chassis |

| Foundation | May vary by age, condition, and setup | May use pier systems, crawl spaces, or permanent foundation options | Typically placed on a crawl space or basement |

| Financing | Can be harder to finance, depending on age and setup | May qualify for chattel loans, manufactured home loans, or conventional loans if on a permanent foundation | Typically qualifies for traditional mortgage financing |

| Insurance | Depends on classification and foundation | May require manufactured home insurance unless permanently installed | Typically uses standard homeowners insurance |

| Long-term value | Often depends on condition, land, and setup | Stronger value potential when properly installed on owned land | Often treated more like a traditional site-built home |

Codes and inspections

Manufactured homes follow HUD standards. Modular homes follow state and local codes and are inspected through the factory and local building process.

That matters because a modular home is reviewed against the building requirements that apply where the home will be installed.

Financing and insurance

Classification matters because lenders and insurers look at how the home is built, titled, installed, and attached to the land. A modular home usually follows a more traditional mortgage and homeowners insurance path.

Manufactured home financing can still be possible, but the details may depend on foundation, title, land ownership, lender requirements, and home type.

Customization and long-term value

Modular homes usually allow broader design changes because they’re built to state and local building codes and placed more like site-built homes. Manufactured homes can offer affordable options, but long-term value often depends on foundation type, land ownership, condition, and maintenance.

For buyers planning to stay long term, those details matter as much as the purchase price.

Choosing the right type starts with your project goals

The right choice depends on how you plan to use the home, not just what the home is called. Compare your budget, land, financing needs, foundation plans, customization goals, and long-term ownership expectations before choosing between manufactured, mobile, and modular homes.

Manufactured or mobile may fit lower upfront budgets

A manufactured home may make sense if affordability is the top priority and the site, zoning, and financing path support that choice. The upfront cost can be lower, but buyers still need to confirm foundation requirements, land ownership, insurance, permits, and lender expectations.

Older mobile homes need a closer look. Age, condition, setup, and local rules can make financing or placement more complicated.

Modular may fit traditional home expectations

A modular home may be a better fit if you want a home that follows state and local building codes, sits on a permanent foundation, and is treated more like a traditional site-built home by lenders and insurers.

This path often fits buyers focused on customization, long-term resale, permanent placement, and a more traditional homeownership process.

How Next Modular supports mobile and modular home buyers

Next Modular helps buyers compare mobile and modular homes through the lens of land, budget, timeline, and project involvement. The key question is how much of the site work and coordination you want to manage yourself.

Home-Only service

Home-Only may suit buyers who already have contractors, construction experience, or a plan to manage the project. Next Modular builds, delivers, and sets the completed custom home, while the buyer generally handles site work, permits, foundation, utilities, and related coordination.

Delivery and setup details can depend on location and project scope, so it’s smart to confirm what’s included before comparing prices.

Turn-Key service

Turn-Key may fit buyers who want a single point of contact where that service is available. Next Modular coordinates the broader project, which may include permits, site preparation, foundation work, utility installation, subcontractor coordination, final inspections, and handoff.

Turn-Key availability depends on location and local Project Manager coverage, so confirm service options early.

What’s the next step?

Once you understand the differences between modular, manufactured, and mobile homes, the next step is matching the right option to your land, budget, timeline, and project needs.

Compare modular home floor plans

Start with modular home floor plans to review layouts, bedroom count, square footage, and customization options. Looking at plans first can help you narrow the kind of home that fits your household before pricing or site planning gets too detailed.

Review Home-Only modular homes

Consider Home-Only modular homes if you plan to manage site work, permits, utilities, and contractors yourself. Buyers with construction support already in place may prefer that level of control over the project.

Ask about Turn-Key modular home service

Ask about Turn-Key modular home service if you want broader project coordination, where available. For buyers who don’t want to manage permits, site prep, utilities, inspections, and handoff alone, Turn-Key can be the more practical path.

Contact Next Modular

For help choosing the right path, contact Next Modular online, call (574) 334-9590, or email [email protected].

Share what you know about your land, budget, timeline, and preferred home type so our team can point you toward the right next step.

Frequently asked questions:

The main difference is the building code. Modular homes follow state and local building codes, while manufactured homes follow federal HUD Code. In technical terms, mobile homes usually refer to older factory-built homes made before modern HUD standards.

Not technically. A mobile home usually refers to a factory-built home made before June 15, 1976. Manufactured homes came after HUD standards, though many buyers still use “mobile home” casually.

Yes. Modular homes are built in factory sections, delivered to the property, and assembled on a permanent foundation. After the home is set, on-site work completes the project.

No. Manufactured homes follow federal HUD Code, while modular homes follow state and local building codes. That difference can affect classification, inspection, financing, insurance, and long-term value.

No. A modular home does not have a permanent steel chassis. It’s built in sections, delivered to the property, and set on a crawl space or basement foundation.

Yes. A manufactured home may be placed on a permanent foundation, depending on the model, site, lender, and local requirements. Buyers should confirm foundation needs before ordering.

Modular homes usually follow a more traditional mortgage path. Manufactured home financing may depend on foundation type, title, land ownership, lender rules, and whether the home qualifies for a specific loan program.

Yes. Modular homes are typically insured through standard homeowners insurance because they’re treated more like traditional site-built homes. Manufactured home insurance may depend on installation and classification.

Modular homes often have stronger resale potential because they follow local building codes and are placed on permanent foundations. Manufactured home value depends more on land ownership, foundation, condition, and market demand.

Manufactured homes are usually more affordable upfront than modular homes. Total project cost still depends on land, site work, foundation, utilities, delivery, setup, permits, and selected upgrades.

Yes. Next Modular specializes in customizable mobile and modular homes, with service options based on buyer needs, home type, project location, and service availability.

Home-Only means the buyer generally manages site work, permits, utilities, and related coordination. Turn-Key means Next Modular coordinates the larger project where that service is available.